Demand for SK Hynix's $28 billion U.S. share sale was more than seven times available shares, a person familiar with the matter said, as the chipmaker prepares to use the money to build new factories and buy equipment for the AI boom. The appetite is huge. The people who make the chips get the cash; the people powering the data centers get the bill in the form of more extraction, more production, more concentration at the top.

Who Holds the Levers

The South Korean chipmaker's offering is set to be the world's second-biggest share sale after SpaceX's record-breaking $85.7 billion IPO last month. SK Hynix declined to comment, and the person who described the demand declined to be identified because the details were confidential. That secrecy fits the usual script. The biggest moves in this system happen behind closed doors, then get sold back to everyone else as market confidence.

The U.S. listing is expected to help SK Hynix narrow its valuation gap with U.S. rival Micron, which, despite having less market share in key memory products, has benefited from direct access to the world's largest pool of investors. Micron currently trades at a 12-month forward price-to-earnings ratio of 6.66 times versus SK Hynix's 5.5 times. Access to capital, not just production, keeps deciding who gets rewarded. The market calls that efficiency.

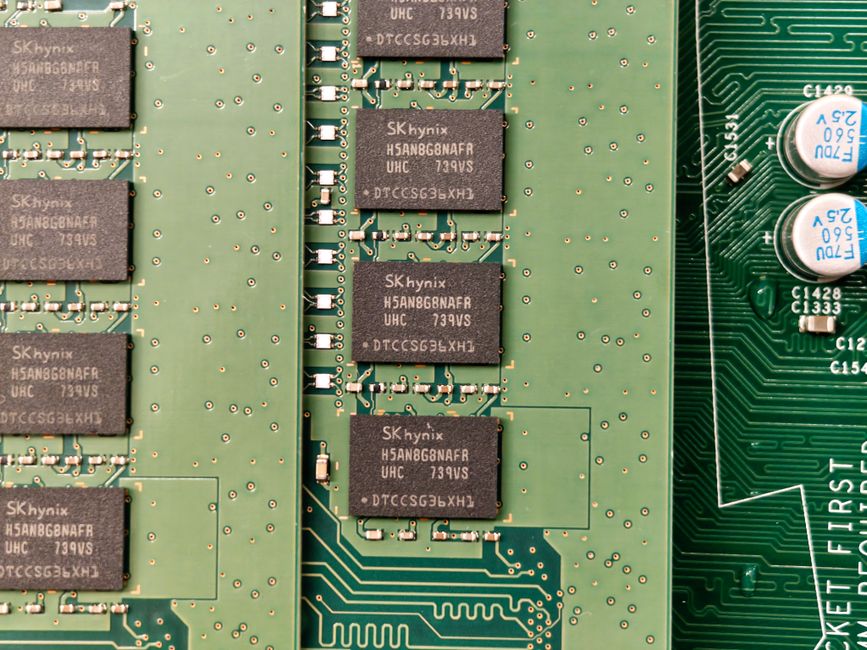

SK Hynix has made its fortune by becoming the most sought-after supplier of high-bandwidth memory chips, the result of 14 years of bets that brought skepticism and scorn but ultimately put it at the centre of the global AI gold rush. Yoo Hoi-jun, an electrical engineering professor at the Korea Advanced Institute of Science & Technology, said, “As long as there is demand for graphic processors and AI data centers, SK Hynix is indispensable.” That word says plenty. Indispensable to the machine, not to the people living under it.

The AI Boom’s Winners

Nvidia CEO Jensen Huang said last month that SK Hynix would continue to be the U.S. AI chipmaker's largest partner, adding that the current memory chip shortage would persist for a few years because of strong demand. Shortage for whom, exactly? For the firms trying to feed the data-center appetite, the problem is supply. For everyone else, the problem is that a handful of corporations and investors get to steer the whole arrangement.

Though shares in semiconductor companies globally have lost momentum in recent weeks, firms like SK Hynix and rival Samsung Electronics are sitting on historic gains as insatiable demand for computer chips to power AI data centres has sent profits soaring. SK Hynix shares closed up 5% on Thursday but have dropped by a quarter in the last two weeks. Even so, the stock is up 680% for the past 12 months. The numbers are obscene in the way only finance can manage: losses for some, historic gains for others, all wrapped in the language of progress.

The firm's profits are so huge that each employee is expected to get an annual bonus of about $574,500, making them highly sought-after marriage partners. That figure lands like a joke told by the system itself. The same machine that squeezes value out of labor can still toss around a number like that and call it normal.

What the Market Calls Fairness

SK Hynix plans to set the final price of the ADR offering on Thursday, and the ADRs will start trading on the Nasdaq on July 10. Ten ADRs will represent one common share, and a Monday filing gave a reference price of 242,500 won per ADR, based on SK Hynix's July 3 closing price in Seoul. On Thursday, the stock closed at 2,186,000 won. The machinery of valuation keeps moving, one filing and one exchange listing at a time, while ordinary people are left to watch the numbers climb.

SK Hynix said that Baillie Gifford Overseas, investment funds managed by Coatue Management and Situational Awareness Partners have each indicated interest in purchasing up to a combined $7 billion of its U.S. ADRs. Big money lines up fast when the returns look rich enough. The names change; the structure doesn't.

Lee Min-hee, an analyst at BNK Investment & Securities, said that contrary to some market expectations, he did not expect SK Hynix's U.S. listing to result in a major boost to its local shares. He said domestic companies still need to contend with the so-called Korea discount, the tendency for them to trade at lower valuations because of concerns about corporate governance. That's the polite language of hierarchy. Investors want access, control, and protection; everyone else gets told the discount is just how the game works.