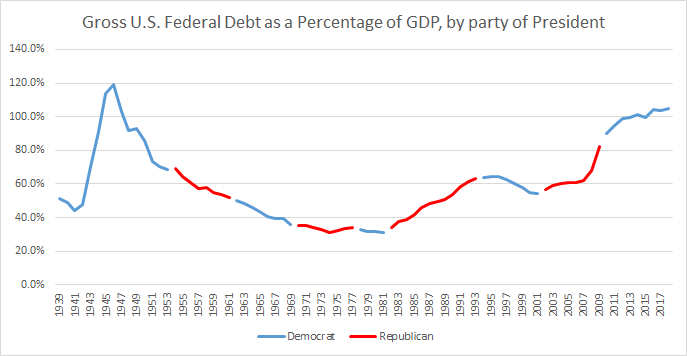

The United States faces mounting fiscal peril as federal debt exceeds 120% of gross domestic product, a near-unprecedented level that threatens to trigger global financial upheaval without serious budgetary reform. The nation has not experienced a bona fide financial crisis since the housing meltdown 19 years ago, and even recent shocks including the Covid pandemic, subsequent inflation surge, and the collapse of Silicon Valley Bank 3 years ago failed to produce financial catastrophe.

Yet this track record may breed dangerous complacency. Financial markets and governments may believe they have acquired immunity, but the world is careening toward a moment of financial upheaval that could dwarf the damage caused by the last one. The most frightening part is not the specific nature of the crisis but the incompetence with which it will be handled, as current US politics practically guarantee that Washington's response will be misguided, steered by Donald Trump's incontinent appetites and animosities.

The Debt Burden

The largest risk revolves around the federal government's accumulation of debt, now in excess of 120% of the nation's gross domestic product and likely to keep growing at a fast clip because of massive built-in budget deficits for the next decade. Maurice Obstfeld, former chief economist at the International Monetary Fund, said: "The political fundamentals are really bad."

The global context compounds the problem. The US's appetite for capital to finance datacenters or the federal deficit is met by China's export of capital to recycle its huge trade surplus. A win-win fix would be for China to spend more on its own stuff while Americans, especially the federal government, spent less, but this seems exceedingly unlikely given politics in Washington and Beijing.

Market Vulnerabilities

Several pathways to crisis exist. One is a financial bubble popping, with stocks buoyed by current euphoria over artificial intelligence being downgraded sharply if returns disappoint, sending the stock market tumbling, shrinking consumer spending and damaging the balance sheets of companies that have piled into the AI dream, as well as their financiers.

It remains unclear what would detonate a sell-off of US government debt, though Treasury bonds still provide the largest, most liquid pool of safe investable assets. Markets were in a tizzy last week, sending rates on government bonds sharply higher over worries about the Iran war and inflation. One year ago, Trump's tariffs on everything sent the price of treasury bonds briefly into a tailspin, evidence that Washington's increasingly idiosyncratic decisions could send investors running for the exit.

The world is not that of 15 years ago, when real interest rates neared zero and central banks in China and many developing countries held massive amounts of treasury bonds, providing a stable source of financing for US deficits. Today, investors buying treasuries want yield and diversification, and they will mercilessly dump US assets if the tide turns sour.

Policy Paralysis

Trump shows no concern over growing federal debt and Republicans in Congress show no interest in stopping him. US politics can still do a lot of damage through scenarios including bombing Iran again, invading Cuba or Greenland, taking control of the Federal Reserve and strong-arming it to cut interest rates, or increasing the deficit through military spending.

The closest anybody in government has come to a plan to address the nation's indebtedness was Scott Bessent, the US treasury secretary, who claimed AI will save the day by generating massive productivity growth and enormous tax revenues to fill the government's coffers. Nobody else has said a word.

If investors freak out and sell off treasuries, raising interest rates on government debt, Trump might strong-arm the Fed to buy the bonds and keep rates low. But pumping that money into the economy would stoke inflation, which would encourage more investors to flee for the exits, sending the dollar into a tailspin. The ideal strategy would be to close the hole in the federal budget. The Fed might force that path by refusing to print money and buy government debt, but Trump is unlikely to appreciate austerity and the odds are slim given his lock on Congress and increasing sway over the Fed.

Obstfeld said: "If you try to war game it, the Fed doesn't have any good options. The only good option is fiscal regime change in the Congress." That is not likely to happen.

France faces the unhelpful combination of a budget crisis and a looming election likely to bring to power a populist right wing that has much in common with Trump's Maga. China, meanwhile, may not face political instability, but it has shown little interest in helping address the imbalances contributing to the world's financial fragility, insisting on subsidizing manufactures for export in order to generate jobs.

In a world where mistrust has strangled space for collective action, damages are likely to be compounded by similarly blinkered responses around the globe. When the crisis hits, international cooperation is unlikely to play much of a role because of the animosities Trump has worked so hard to kindle. The world is staring into an unprecedented future in which a financial crisis like the world has never seen invites the most self-defeating government response ever.

Why This Matters:

Fiscal discipline remains the cornerstone of economic stability and national sovereignty. With federal debt exceeding 120% of GDP and massive built-in deficits projected for the next decade, the United States faces a credibility crisis that threatens its position as the anchor of global finance. Treasury bonds have historically provided the world's safest investable assets, but today's investors demand yield and will abandon US debt if fiscal recklessness continues unchecked. The absence of any serious plan to address indebtedness—beyond speculative claims about AI-driven revenue growth—signals a dangerous abdication of fiscal responsibility. Without congressional action to restore budgetary discipline, the Federal Reserve faces impossible choices between enabling inflation or forcing a painful economic correction. The stakes extend beyond domestic markets: a US debt crisis would reverberate globally, and current political divisions make coordinated international response unlikely.